The Pag-IBIG MP2 Savings Program (Modified Pag-IBIG II) is one of the most popular voluntary savings schemes in the Philippines today. It is designed for members of the Home Development Mutual Fund (HDMF or Pag-IBIG Fund) who wish to grow their money in a safe, government-backed, and higher-yield investment program compared to regular Pag-IBIG I contributions. Since its launch, MP2 has attracted millions of Filipinos—both locally and abroad—because of its higher dividends, flexible terms, and tax-free earnings.

But before one can start investing in MP2, there are specific requirements and qualifications that need to be understood. These requirements are not just limited to documents but also cover membership eligibility, financial capacity, and compliance with Pag-IBIG regulations. Below is a detailed breakdown of what’s needed to participate in MP2.

Eligibility Requirements

The very first step is determining who can invest in MP2. Not everyone can immediately join, since the program is exclusively offered to Pag-IBIG members and former members who meet the following conditions:

- Active Pag-IBIG I Members

- An individual must be an active contributor to the regular Pag-IBIG I program.

- This means the member has at least one (1) monthly contribution under Pag-IBIG I within the last six months.

- Salaried employees, self-employed individuals, freelancers, and professionals can all be considered active members as long as they remit their Pag-IBIG contributions.

- Former Members with 24 Months of Contributions

- Retirees or separated members who have already accumulated at least 24 monthly contributions in Pag-IBIG I are also eligible.

- This condition makes MP2 attractive to retirees, since even without active employment, they can continue saving through MP2 and earn passive income from dividends.

- OFWs (Overseas Filipino Workers)

- OFWs who are Pag-IBIG members can also invest in MP2.

- Many OFWs actually prefer MP2 because it allows them to safely save and grow money while working abroad.

In short, the basic eligibility requirement is simple: you must be either an active Pag-IBIG I contributor or a former member with at least 24 contributions.

Documentary and Account Requirements

Once eligibility is confirmed, the next step is to comply with the account opening requirements:

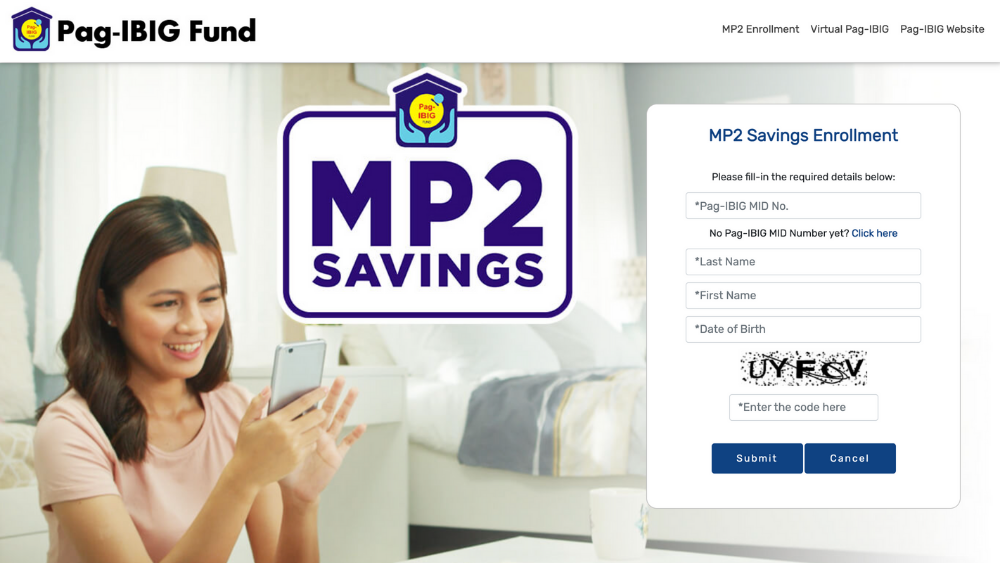

Pag-IBIG MID Number (Membership ID)

Every MP2 enrollee must have a Pag-IBIG Membership Identification Number.

Without this unique ID, it is impossible to open an MP2 account.

If a member does not have one, they need to register first as a Pag-IBIG I member.

MP2 Enrollment Form

Members must accomplish the official Modified Pag-IBIG II Enrollment Form, which can be downloaded from the Pag-IBIG website or filled out online via the Virtual Pag-IBIG portal.

The form requires details such as personal information, Pag-IBIG MID number, source of income, preferred dividend payout option (annual or compounded), and nominee information in case of death.

Valid IDs

At least one valid government-issued ID (passport, driver’s license, UMID, PRC license, etc.) is required for verification.

For OFWs applying abroad, scanned copies of IDs may be submitted online or through authorized remittance partners.

Initial Savings (Minimum Contribution)

The minimum amount to start an MP2 account is ₱500.

Members can deposit their savings through salary deduction (if arranged with an employer), over-the-counter at Pag-IBIG branches, partner banks, or digital channels such as GCash, PayMaya, and Virtual Pag-IBIG.

Nominee / Beneficiary Information

Members are required to indicate at least one beneficiary or heir in the event of death.

This ensures that the savings and dividends will be transferred to the rightful person.

Financial Requirements and Contributions

While the minimum deposit requirement is only ₱500, members should understand the following financial rules:

- No maximum limit – Unlike many investment vehicles, Pag-IBIG MP2 has no cap on the amount of savings. A member can deposit ₱500 monthly or even millions in one lump sum.

- Lock-in period of 5 years – All MP2 savings are locked in for five years, which means you cannot withdraw until maturity (except under special circumstances like disability, retirement, or death).

- Dividend earnings – MP2 dividends are based on Pag-IBIG’s net income, declared annually, and are tax-free. On average, dividends range from 6% to 8% per year, making it one of the highest-yielding government-guaranteed savings programs.

- Modes of dividend payout – Members can choose between:

- Annual dividend payout – Dividends are credited yearly to a savings account or remittance channel.

- Compounded dividends – Dividends are added to the principal and rolled over until maturity, resulting in higher earnings after 5 years.

Process of Opening an MP2 Account

Here’s a step-by-step outline of how requirements are used in practice:

- Secure your Pag-IBIG MID number.

- Fill out the MP2 Enrollment Form (online or at a branch).

- Present a valid government ID for identity verification.

- Submit the form to Pag-IBIG (or apply via Virtual Pag-IBIG).

- Make your initial ₱500 savings deposit through your preferred payment channel.

- Receive your MP2 account number, which you will use for subsequent deposits.

Special Considerations

- Multiple Accounts – A member can open more than one MP2 account, useful for those who want to separate savings goals (e.g., retirement fund, education fund, emergency fund).

- Early Withdrawal – While discouraged, early withdrawal of savings is allowed under cases of total disability, retirement, unemployment, or death. However, withdrawing voluntarily before maturity may result in reduced dividend earnings.

- For Corporate/Employer Contributions – Some companies allow salary deduction for MP2, making it easier for employees to save regularly.

Conclusion

The requirements for enrolling in Pag-IBIG MP2 are simple, accessible, and flexible. At its core, the primary conditions are being a Pag-IBIG member (active or former with 24 contributions), having a Pag-IBIG MID number, accomplishing the MP2 enrollment form, presenting a valid ID, and making an initial minimum ₱500 contribution. Compared to private investment options, the barriers to entry are very low, making MP2 one of the most inclusive financial programs available to Filipinos.

By meeting these requirements, members gain access to a government-guaranteed, tax-free, and high-yield savings program that can significantly help in retirement planning, education funding, or wealth accumulation. MP2 is proof that even with a modest monthly contribution, Filipinos can take a big step toward financial security, provided they understand and comply with the simple requirements set by Pag-IBIG.

Other related articles

Is MP2 better than a savings account?

100k one time deposit in pag-ibig mp2, how much after 5 years?

What will happen to MP2 after 5 years?

How much can I earn in pag-ibig mp2 savings if I invest 2,000 pesos monthly?

Ang Pag-IBIG Loyalty Plus Card ay mahalaga dahil nagbibigay ito ng maraming benepisyo sa mga miyembro ng Pag-IBIG Fund. Narito Read more

Oo, maaaring pumunta sa Embassy o Consulate ng Pilipinas sa ibang bansa upang humingi ng tulong sa pag-unlock ng iyong Read more

Ang Pag-IBIG MP1 at MP2 ay magkahiwalay na programa dahil sa kanilang magkaibang layunin, benepisyo, at istruktura. Narito ang mga Read more

Kapag ang may-ari ng isang Pag-IBIG MP2 account ay namatay, ang pamilya o mga tagapagmana ay maaaring mag-claim ng savings Read more