The Pag-IBIG MP2 Savings Program is one of the most popular voluntary savings options in the Philippines because of its relatively high dividend rates compared to regular banks. If you put money into MP2, your savings are locked for five years, and after that period, you have several choices depending on your financial goals. Let’s break it down in detail to see what will happen to your MP2 after 5 years.

1. Maturity of Your MP2

When you open an MP2 account, you agree to keep your money with Pag-IBIG for five years. This period is called the maturity period. After five years, the account is considered matured, which means:

- Pag-IBIG will stop crediting new dividends to that account unless you take action.

- You will be notified (through email, SMS, or Pag-IBIG office channels) that your account has reached maturity.

- You will have to choose whether to withdraw the money or roll it over into a new MP2 account.

2. Options After Maturity

a. Withdraw All Your Savings + Dividends

The most straightforward option is to withdraw everything you’ve earned. This includes:

- Your original capital (all the deposits you made for five years).

- The total dividends credited during that time.

The dividends depend on how Pag-IBIG’s funds performed. Historically, MP2 dividends range from 6% to 8% annually, though this is not guaranteed. If you choose annual dividend payout, you would have already received the dividends every year in your bank account or through check. If you chose the compounded dividend option, then both your savings and dividends will be released to you as a lump sum after five years. This second option usually gives higher returns because of compounding.

b. Rollover into Another 5-Year Term

If you don’t need the money yet and want to continue growing it, you can roll over your savings into a new MP2 account. This means opening a new MP2 account and transferring the matured funds there. The cycle then starts again with a new 5-year term.

This is a common choice for people who want to treat MP2 as a medium-term investment vehicle and don’t have immediate plans for the money.

3. What If You Don’t Do Anything?

If you simply leave the money in your MP2 account after 5 years without withdrawing or rolling over:

- Your funds will stop earning dividends after the maturity date.

- The money will just sit idle with Pag-IBIG, similar to a dormant account.

- Eventually, Pag-IBIG will still release the money to you once you claim it, but you lose the potential growth from dividends during the idle years.

This is why it’s important to take action once your MP2 matures.

4. Strategic Considerations

What you do after 5 years depends on your financial needs:

- If you need liquidity (money for business, education, home, etc.), it makes sense to withdraw.

- If you want to keep growing wealth, reinvesting or rolling over to another MP2 term is smarter.

- Some people open multiple MP2 accounts in different years (staggered approach). That way, one account matures every year, giving them flexibility to either withdraw or reinvest gradually.

5. Example Scenario

Let’s say you deposited ₱1,000 per month for 5 years (₱60,000 total contributions). If the average dividend rate is around 7% per year and you chose compounding, your account could grow to around ₱70,000–₱75,000 or more after 5 years. Upon maturity:

- You can withdraw the ₱75,000 in full.

- Or roll it into a new MP2 account to continue earning dividends for another 5 years.

Conclusion

After 5 years, your MP2 savings will mature, and you’ll need to decide whether to withdraw your money or roll it into another 5-year term. If you withdraw, you gain access to both your savings and the dividends earned. If you roll it over, your money continues to grow. However, if you do nothing, the account stops earning dividends, which means you’re missing out on potential earnings. The best choice depends on your financial goals, but the key is to plan ahead so your money keeps working for you.

Other related articles

How much can I earn in pag-ibig mp2 savings if I invest 2,000 pesos monthly?

Can I withdraw my Pag-IBIG MP2 annually?

What are the disadvantages of pag-ibig mp2?

How to apply Pag ibig Mp2 for ofw online

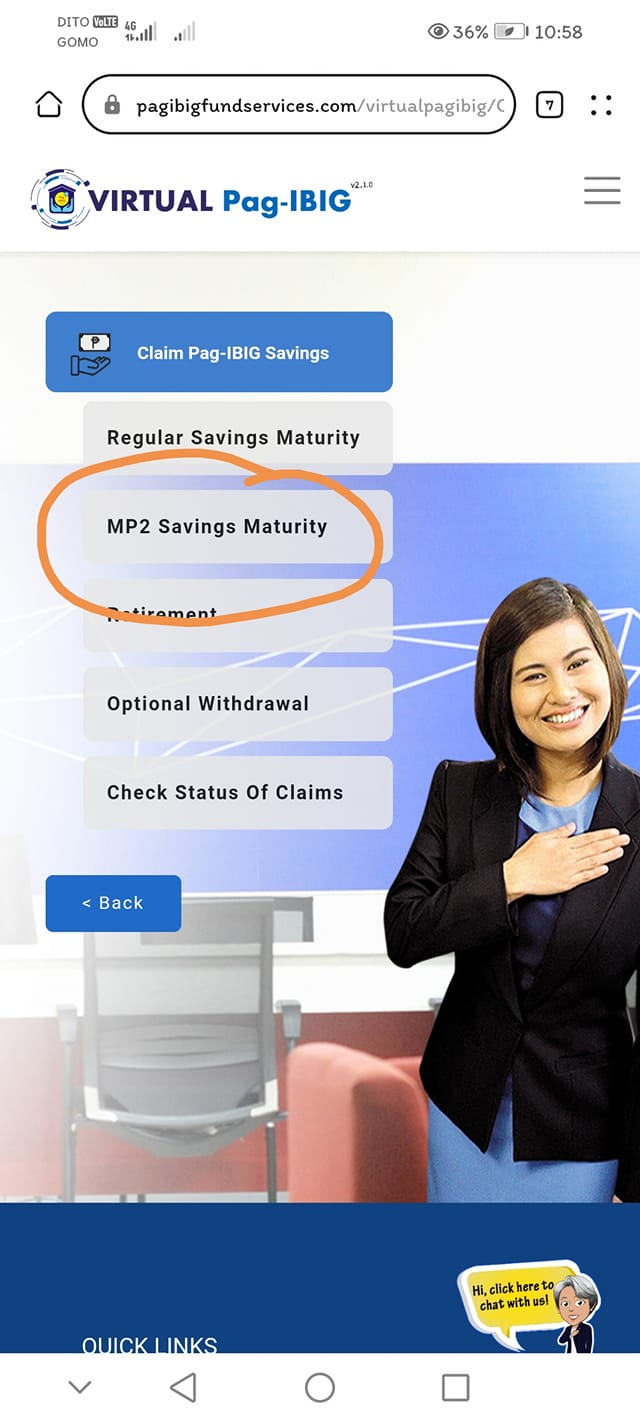

Para malaman kung pwede mo nang i-claim ang maturity ng iyong Pag-IBIG MP2 account, maaari mong gamitin ang Pag-IBIG Virtual Read more

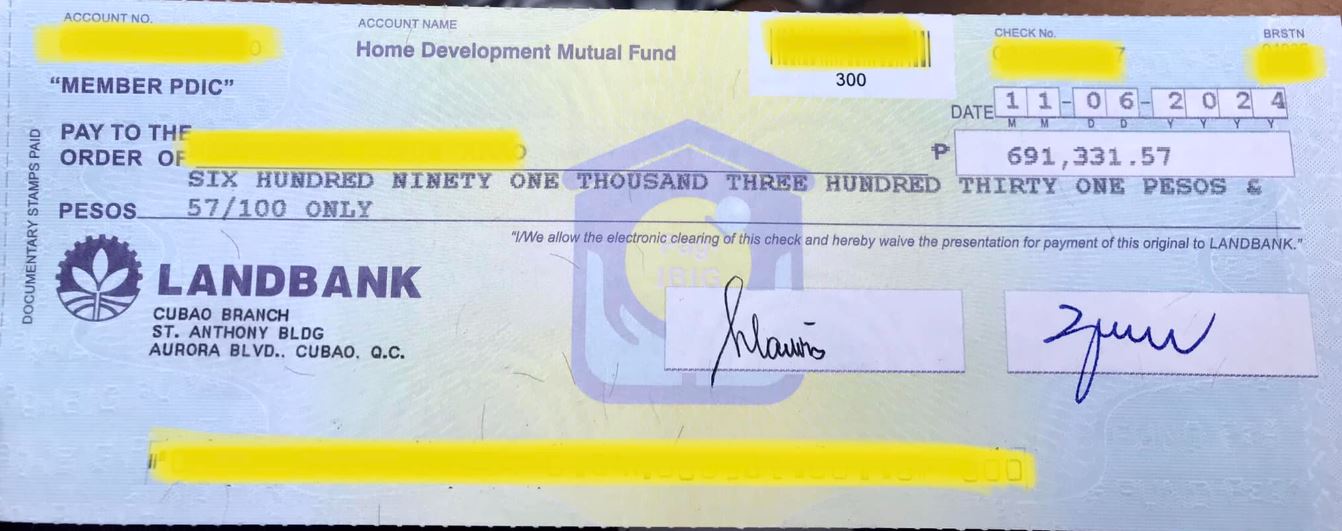

Oo, maaari mong i-encash ang iyong Pag-IBIG MP2 check sa ibang branch ng Land Bank of the Philippines (LANDBANK) kahit Read more

Ang tagal ng pag-release ng cheque ng Pag-IBIG MP2 ay depende sa proseso ng Pag-IBIG Fund, ngunit karaniwang tumatagal ito Read more

Hindi mo na kailangan ng proof of income para ma-withdraw ang iyong MP2 savings, kahit na ang accumulated savings mo Read more