Pag-IBIG MP2 is a government-backed voluntary savings program created by the Home Development Mutual Fund (HDMF) of the Philippines. It is designed to provide higher annual dividends than the regular Pag-IBIG I membership program. The MP2 Savings Program has a fixed 5-year maturity period, during which members can grow their savings with compounded or annual dividend payouts. It is tax-free, safe, and open to all active Pag-IBIG Fund members, including Overseas Filipino Workers (OFWs). For OFWs looking for a reliable investment option, MP2 offers a smart and secure opportunity to build wealth.

Who Can Apply?

OFWs can apply for the MP2 Savings Program if they are active Pag-IBIG I members with at least one monthly contribution in the last six months. Even former members who have made a total of at least 24 contributions are eligible. Applicants must possess a valid Pag-IBIG MID number and an active email address. This flexibility makes MP2 accessible to both current and past contributors. The program supports OFWs’ financial goals by offering a low-entry, high-dividend saving option.

An OFW can apply for MP2 if:

- You are a Pag-IBIG I member with at least one monthly contribution in the last 6 months.

- OR a former Pag-IBIG member with at least 24 total contributions.

- You have a Pag-IBIG MID number.

- You have a valid email address and internet access.

How to Apply for Pag-IBIG MP2 Online (For OFWs)

Applying online for MP2 is simple and can be done from anywhere in the world. The online enrollment system is streamlined for OFWs, removing the need to visit a local Pag-IBIG office. All you need is a stable internet connection, your Pag-IBIG MID number, and accurate personal and contact details. With these, you can easily navigate through the MP2 enrollment process online.

Step 1: Go to the MP2 Enrollment Website

To begin, visit the official Pag-IBIG MP2 Enrollment Portal at https://www.pagibigfundservices.com/MP2Enrollment/. This is the designated platform where you will initiate your application. It’s optimized for both desktop and mobile use, making it easy for OFWs to apply even on the go. Make sure you’re on a secure internet connection to safeguard your personal information during the process.

Step 2: Enter Your Pag-IBIG MID Number

Once you’re on the enrollment page, enter your valid Pag-IBIG MID number—not the tracking number. This ensures that the system can verify your membership status. Provide your full name and birthdate exactly as registered with Pag-IBIG. Upon submission, the system will confirm if your MID number is active and will guide you to the next step.

Step 3: Complete the Online Enrollment Form

This part of the process involves providing additional personal and employment information. You’ll need to input your overseas and Philippine addresses, active mobile number, and valid email. You’ll also choose your dividend payout option (compounded or annual) and preferred payment method. You may optionally list your beneficiaries. This form is crucial, as it determines how your savings will be managed over the 5-year period.

Step 4: Submit and Save Your MP2 Account Number

After completing the form, submit it and wait for your MP2 Savings Account Number to be generated. This number is unique to your MP2 account and must be used for all future transactions. You’ll receive a downloadable enrollment form and a confirmation email. Be sure to save a copy of both for your records.

How to Send MP2 Contributions from Abroad

OFWs have multiple options for remitting contributions to their MP2 accounts. The minimum contribution is PHP 500 per remittance, and there’s no maximum limit. You can use Virtual Pag-IBIG, GCash, PayMaya, remittance partners, or online banking platforms. This flexibility ensures that OFWs from any country can make regular contributions conveniently.

Payment Options for OFWs:

- Virtual Pag-IBIG Portal

- Go to: https://www.pagibigfundservices.com/VirtualPagibig/

- Pay via GCash, PayMaya, Visa, or MasterCard

- GCash / PayMaya (If available abroad)

- Bills Payment → Government → Pag-IBIG MP2

- Overseas Remittance Partners

- iRemit, AUB, RCBC TeleMoney, Ventaja, Metrobank, BDO Kabayan, etc.

- Use your MP2 account number as the reference

- OFW Online Banking / Philippine Banks

- Log in to your Philippine online banking account

- Choose Bills Payment → Pag-IBIG MP2

- Input your MP2 Account Number

Payment Options for OFWs

Pag-IBIG provides several channels to make MP2 contributions seamless for OFWs. Through the Virtual Pag-IBIG portal, you can pay using GCash, PayMaya, or even credit/debit cards. Alternatively, remittance centers like iRemit, RCBC TeleMoney, and Ventaja allow payments through authorized partners abroad. You can also use Philippine bank accounts with online banking for bills payment.

How to Monitor Your MP2 Account Online

To keep track of your savings, dividends, and account history, sign up for the Virtual Pag-IBIG portal. It’s a secure online platform that provides 24/7 access to your account information. After verifying your identity with a valid ID and selfie, you can log in and check your MP2 account anytime. This tool empowers OFWs to monitor their investments even while abroad.

Use the Virtual Pag-IBIG portal to track your contributions and dividends:

- Sign up: https://www.pagibigfundservices.com/virtualpagibig/

- Upload valid ID and photo for verification

- Check your MP2 balance, history, and personal info

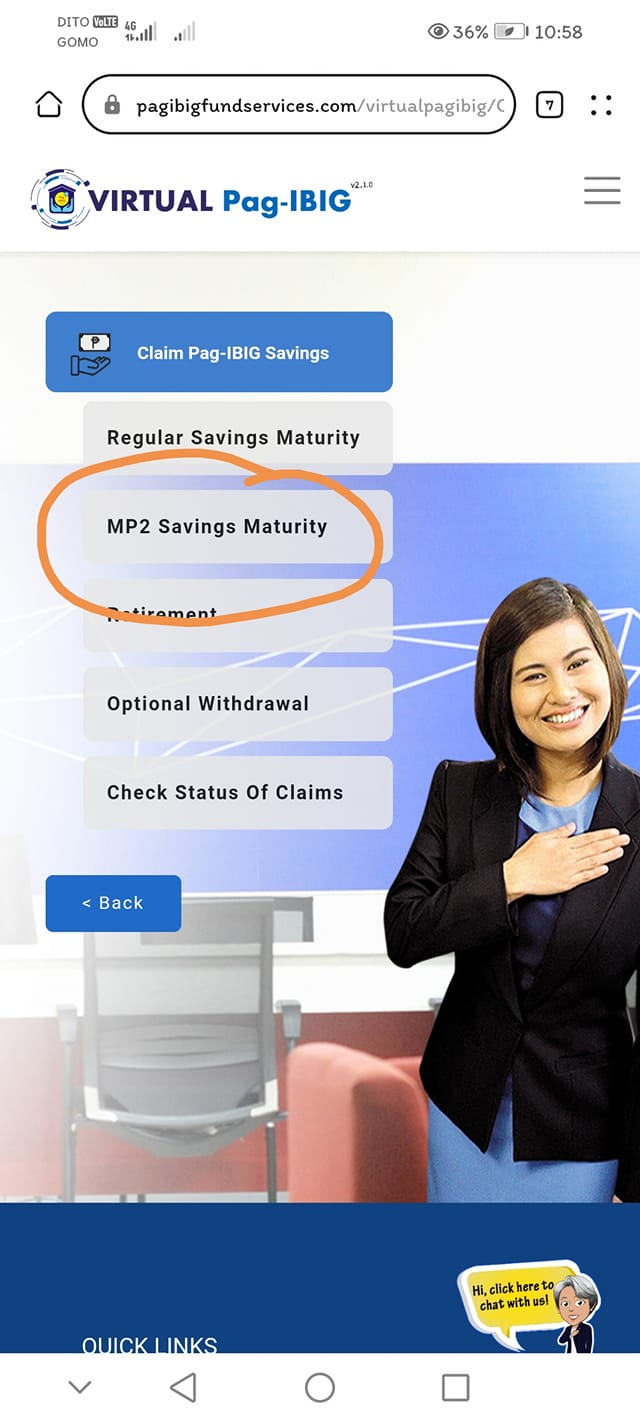

When and How to Withdraw MP2 Savings

After the five-year maturity period, you can withdraw your entire savings and earned dividends. Choose to receive the payout via bank credit or check. If you’re still working abroad, you can request withdrawal through Virtual Pag-IBIG or authorize a trusted person in the Philippines to process it. Early withdrawals are allowed under specific conditions like disability, retirement, or severe illness.

Your savings mature after 5 years. At that point, you can:

- Withdraw your total contributions plus earned dividends

- Choose payout via bank credit or check (for pickup)

If you’re still abroad, you can file via Virtual Pag-IBIG or authorize someone in the Philippines.

Important Notes for OFWs

MP2 is highly flexible—there’s no penalty for skipping contributions, and members can open multiple MP2 accounts. All dividends are tax-free and government-guaranteed. It’s ideal for long-term savings, especially for goals like retirement, property investment, or children’s education. MP2 is widely regarded as one of the most secure and profitable savings options for Filipinos overseas.

You can skip contributions—MP2 is voluntary

You may open multiple MP2 accounts

Dividends are tax-free and guaranteed

Early withdrawals are allowed for:

- Disability, death, critical illness, or retirement

Pag-IBIG Overseas Contact Channels

Should you have questions or need help with your account, Pag-IBIG offers various overseas support channels. You can email them at contactus@pagibigfund.gov.ph or use the Virtual Assistant on their official website. Their Facebook page (@PagIBIGFundOfficial) is also active for general inquiries. For country-specific assistance, check the directory of foreign posts listed on their website.

Summary

The MP2 online enrollment process is quick, easy, and perfect for OFWs. From getting your MP2 number to choosing your preferred mode of contribution, every step can be done online. With the Virtual Pag-IBIG portal, you can track your savings and apply for withdrawal when your term ends. It’s a reliable and efficient way for OFWs to grow their money while securing their future.

| Step | Description |

|---|---|

| 1 | Visit MP2 Online Enrollment |

| 2 | Enter your Pag-IBIG MID number |

| 3 | Complete the MP2 enrollment form |

| 4 | Submit and receive your MP2 account number |

| 5 | Start saving via remittance, online, or Virtual Pag-IBIG |

| 6 | Track your account using the Virtual Pag-IBIG portal |

Final Tips

Consider using the compounded dividend option to maximize your earnings. Set a regular contribution schedule that fits your budget. Use authorized payment channels to ensure proper posting of your savings. Don’t forget to renew or reinvest after maturity. MP2 is not only a smart savings strategy but also a step toward financial freedom for OFWs and their families.

Other Related Articles

Do I need to deposit monthly in MP2?

What will happen if I stop paying my Pag-IBIG contribution?

How to qualify for MP2 Pag-IBIG?

Can I withdraw my Pag-IBIG MP2 anytime?

Oo, puwedeng magbukas ng dalawa o higit pang MP2 accounts para sa isang tao lamang. Walang limitasyon sa dami ng Read more

Oo, ang Pag-IBIG MP2 ay nagbibigay ng notification kapag na-reach na ang maturity ng iyong account. Gayunpaman, ang notification ay Read more

Kapag ikaw ay naging Australian citizen o dual citizen, maaari ka pa ring mag-contribute sa Pag-IBIG Fund at magbukas ng Read more

Para malaman kung pwede mo nang i-claim ang maturity ng iyong Pag-IBIG MP2 account, maaari mong gamitin ang Pag-IBIG Virtual Read more

Pingback: What are the disadvantages of pag-ibig mp2? – Pag-ibig MP2 FAQS